Home buyers with weak cost savings for a deposit are an excellent fit for an FHA loan. The FHA has a number of requirements for home loan. Initially, the majority of loan amounts are limited to $417,000 and do not supply much flexibility. FHA loans are fixed-rate home mortgages, with either 15- or 30-year terms. Purchasers of FHA-approved loans are also required to pay home loan insurance coverageeither upfront or over the life of the loanwhich hovers at around 1% of the cost of your loan quantity.

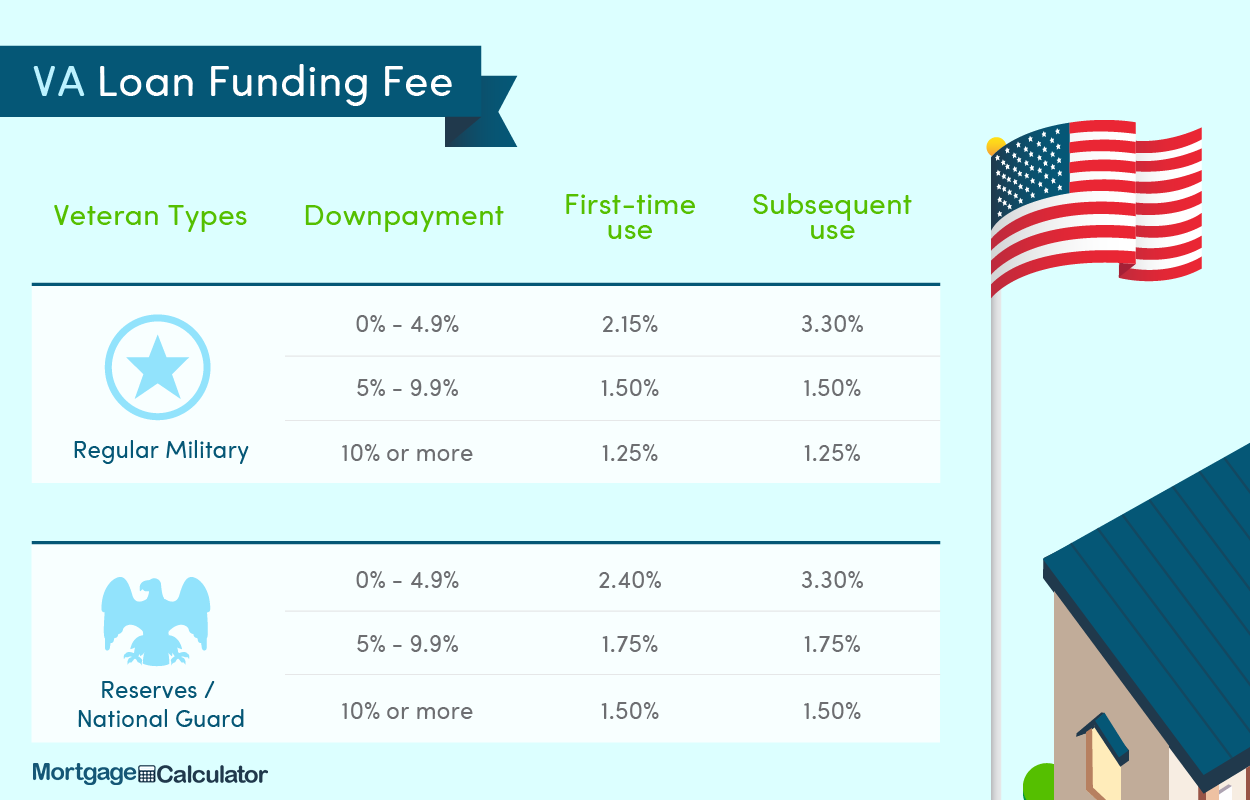

If you qualify for a VA loan, you can score a sweet home with no deposit and no home loan insurance requirements. VA loans are for veterans who've served 90 days consecutively during wartime, 180 throughout peacetime, or 6 years in the reserves. Since the home loans are government-backed, the VA has stringent requirements on the kind of house buyers can buy with a VA loan: It needs to be your main residence, and it should fulfill "minimum home requirements" (that is, no fixer-uppers enabled). Another government-sponsored mortgage is the USDA Rural Advancement loan, which is developed for families in backwoods.

Debtors in rural locations who are struggling financially can access USDA-eligible house loans. These home mortgage are designed to put homeownership within their grasp, with budget friendly mortgage payments. The catch? Your financial obligation load can not surpass your earnings by more than 41%, and, similar to the FHA, you will be required to buy home mortgage insurance coverage.

Lenders will wrap your existing and new home mortgage payments http://zanderzbdp122.trexgame.net/how-are-adjustable-rate-mortgages-calculated-things-to-know-before-you-buy into one; as soon as your home is sold, you pay off that home mortgage and re-finance. Property owners with exceptional credit and a low debt-to-income ratio, and who don't require to finance more than 80% of the 2 homes' combined worth. Meet those requirements, and this can be a basic way of transitioning between two homes without having a meltdownfinancially or emotionallyin the procedure.

No matter what your home loan requirements may be, there is a proper loan offered for you. Utilize this useful guide to help understand the various types of home mortgages available to homebuyers - what is the maximum debt-to-income ratio permitted for conventional qualified mortgages. A fixed-rate home loan will lock you into one rates of interest for the entire regard to your mortgage. The advantage of this is monthly payment security over the length of your mortgage.

An adjustable rate home mortgage generally adjusts the loan's rates of interest as soon as a year, and locks into that rate for the totality of the year. ARMs are typically riskier since the payments can increase depending on rate of interest. The goal of an ARM is to take advantage of the most affordable interest rates available, presuming your income may increase in time as the rate of interest potentially changes upward.

Getting My What Is The Highest largest timeshare companies Interest Rate For Mortgages To Have a peek here Work

An intermediate or hybrid home loan starts as a set rate home loan for a number of years, and after that ends up being adjustable. 10/1 ARM: In this ARM, the rates of interest is repaired for the first ten years of the loan, and after that ends up being adjustable every year going forward. 5/1 ARM: This works the like a 10/1 ARM, but the loan would become adjustable after 5 years.

There are typically some restrictions, like only being able to lock in within the very first 5 years. This is different from refinancing, since you will not have the alternative to change again, however instead will be locked in. Securing to a set rate may sustain a charge or have a cost connected with it.

You will usually need to have excellent credit, an appropriate debt-to-income ratio to support a big loan, and the down payment will be significant since of the expense of the house. Payments made on a balloon mortgage will normally be lower than average, and in many cases will just be interest payments.

This results in a large payment at the end of a relatively short-term. These mortgages are usually taken out commercially, and are taken out by those preparing to sell a property in the near future. A loan with absolutely no deposit offered only to veterans. The deposit for a VA home loan is assisted by the VA.

This loan is great for very first time home buyers, those that can't pay for a routine deposit, or those with poor credit. If you can afford a 5% down payment, opt for a traditional loan to get a better interest rate. For more details and aid comprehending the various types of mortgages that might be a great fit for you, call among our Pentucket Bank Home Loan Officers.

We always keep servicing of our loans, so you can always reach us locally for concerns during the life of your loan. Send us an e-mail or offer us a call today at (978) 372-7731 to find out how we can assist you as you consider your home loan alternatives.

Not known Factual Statements About What Is The Going Rate On 20 Year Mortgages In Kentucky

Now is a fun time to do some research study to better comprehend the types of loans that are readily available to you. When you're all set to go out in the market, you'll feel more positive understanding which one is the right type for you. One of the initial steps in buying a brand-new house is deciding how you'll fund it.

There are numerous kinds of home mortgage offered, so you can choose the home loan program that finest suits your monetary situation. A home mortgage loan officer can assist you arrange through your choices, but here are some of the essentials to help get you started. When you're comparing different types of home mortgages, you need to look at these essential points: Home requirements Debtor requirements How home loan payments are structured Not all kinds of home loans will work for all purchasers, so it's helpful to speak with your lender to sort through the finest option for you, particularly after discovering the current federal rate cuts due to COVID-19 (what income is required for mortgages in scotland).

The matter of fixed-rate versus adjustable-rate home loans will enter into play with almost all types of home mortgage programs. As the name suggests, a fixed-rate home loan is one that preserves the exact same interest rate throughout the life of the loan. With an variable-rate mortgage (ARM), the interest rate can alter after the initial fixed-rate period, which might be between 1-10 years.